The Importance of Preparing for Your Family’s Golden Years

Embarking on retirement planning for families is a proactive and profoundly collaborative process designed to ensure the financial stability and holistic well-being of all family members during their post-working years. Unlike individual planning, family-centric retirement preparation navigates unique complexities, encompassing considerations for children’s education, elder care, and establishing a lasting legacy. It’s about crafting a shared vision for the future, fostering intergenerational security, and minimizing financial stress across the household. A well-constructed plan provides peace of mind, allowing families to enjoy their later years with confidence and freedom.

Understanding the Core Principles of Family Retirement Planning

Effective household retirement preparation begins with a clear grasp of foundational principles that guide every decision. These principles ensure that a family’s financial roadmap is not only robust but also adaptable to life’s inevitable changes.

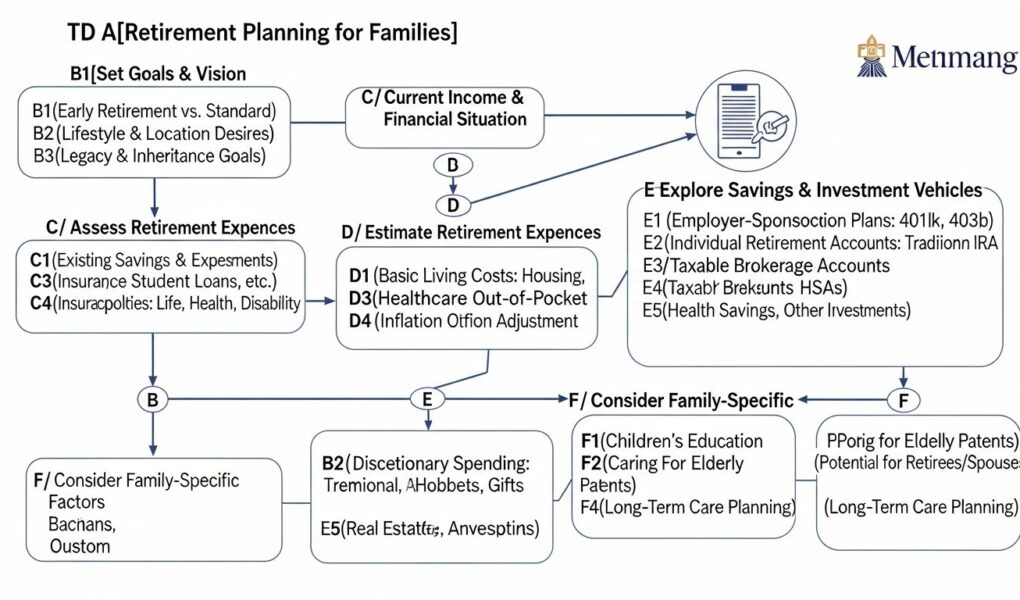

- Setting Shared Family Retirement Goals: This involves open communication among spouses and, where appropriate, older children, to define a collective vision for retirement. What lifestyle do you envision? Will you travel, pursue hobbies, or support philanthropic causes? Establishing realistic, measurable, and time-bound goals forms the bedrock of your strategy.

- Assessing Family Risk Tolerance: Understanding the collective comfort level with investment risk is crucial. A family’s risk tolerance might differ from an individual’s, factoring in dependents, outstanding debts, and job stability. This assessment informs asset allocation decisions, balancing growth potential with security.

- Accounting for Inflation and Time Horizon: The purchasing power of money diminishes over time due to inflation. A plan must anticipate future costs for living expenses, healthcare, and leisure. The time horizon—how many years until retirement—dictates the aggressiveness of investment strategies, with longer horizons typically allowing for more growth-oriented approaches.

- The Power of Diversification: Spreading investments across various asset classes (stocks, bonds, real estate) and geographies minimizes risk. Diversification ensures that a downturn in one area does not derail the entire portfolio, safeguarding your family’s financial future.

See our detailed guide on Core Principles of Family Financial Planning.

| Section | Key Focus | Family Benefit |

|---|---|---|

| Introduction | Defining family retirement planning & its importance | Holistic financial stability & well-being |

| Core Principles | Goal setting, risk, inflation, diversification | Robust & adaptable financial roadmap |

| Financial Vehicles | 401(k), IRA, 529, life insurance, etc. | Optimized savings & growth with tax advantages |

| Unique Family Needs | Children’s education, elder care, legacy | Comprehensive protection for all dependents |

| Tax Implications | Tax-deferred vs. tax-free growth | Maximizing net retirement income |

| Common Mistakes | Pitfalls like underestimating costs, delayed start | Avoiding costly errors in planning |

| Building a Plan | Step-by-step guide to plan creation | Structured approach to financial security |

| Review & Adapt | Regular adjustments to life changes | Ensuring long-term plan relevance & effectiveness |

[INLINE IMAGE 1: a diagram showing a multi-generational family (parents, children, grandparents) collaboratively discussing financial documents at a kitchen table, symbolizing shared financial planning]

Key Financial Vehicles for Family Retirement Savings

To effectively achieve your family’s retirement goals, understanding and utilizing the right financial vehicles is paramount. These instruments offer varying benefits, particularly in terms of tax advantages, contribution limits, and withdrawal rules, making it essential to select those best suited for your household’s specific needs.

How Do 401(k)s and IRAs Benefit Families?

Employer-sponsored 401(k) plans and individual retirement accounts (IRAs) are cornerstones of individual and family retirement savings. 401(k)s often come with employer matching contributions, which are essentially free money, significantly boosting savings. Both Traditional 401(k)s and IRAs offer tax-deferred growth, meaning contributions might be tax-deductible now, and taxes are paid upon withdrawal in retirement. This can be beneficial for families currently in higher tax brackets, allowing more money to grow uninterrupted. Spousal IRAs also allow a non-working spouse to save for retirement, provided their partner has earned income, enabling two separate retirement income streams for the family.

What Are the Tax Advantages of a Roth IRA for Households?

Roth IRAs provide a compelling alternative, particularly for younger families or those who anticipate being in a higher tax bracket during retirement. Contributions to a Roth IRA are made with after-tax dollars, but qualified withdrawals in retirement are entirely tax-free. This offers incredible flexibility and predictability, as your family won’t have to worry about future tax rates on their retirement income. For families contributing to both traditional and Roth accounts, a diversified tax strategy can emerge, providing options for tax-efficient withdrawals later in life.

Other vital instruments for securing a family’s golden years include 529 plans for college savings, annuities for guaranteed income streams, and taxable brokerage accounts for flexible, non-retirement-specific investments. Life insurance and long-term care insurance also play crucial roles in protecting family assets and ensuring care needs are met without depleting retirement funds.

| Account Type | Primary Benefit for Families | Tax Treatment (Contributions) | Tax Treatment (Withdrawals) | Contribution Limits (2026) | Best For (Specific Family Scenario) |

|---|---|---|---|---|---|

| 401(k) | Employer match, high limits, tax-deferred growth | Pre-tax (Traditional), After-tax (Roth) | Taxable (Traditional), Tax-free (Roth, qualified) | $23,000 (plus catch-up for 50+) | Families whose employers offer a match, maximizing savings |

| Traditional IRA | Tax-deductible contributions, tax-deferred growth | Pre-tax (may be deductible) | Taxable | $7,000 (plus catch-up for 50+) | Families seeking current year tax deductions |

| Roth IRA | Tax-free withdrawals in retirement | After-tax | Tax-free (qualified) | $7,000 (plus catch-up for 50+) | Younger families expecting higher future tax rates |

| 529 Plan | Tax-advantaged college savings | After-tax | Tax-free (qualified education expenses) | Varies by state, often very high | Families saving for children’s future education costs |

| Annuity | Guaranteed income stream in retirement | After-tax | Taxable (earnings portion) | No federal limit | Families seeking predictable, lifetime income |

| Taxable Brokerage Account | Flexible access to funds, no contribution limits | After-tax | Capital gains taxed | No federal limit | Families needing liquid assets or exceeding other limits |

See our detailed guide on Choosing the Right Retirement Accounts for Your Family.

Addressing Unique Family Needs in Retirement Planning

Intergenerational retirement planning extends beyond personal savings to encompass the diverse needs of all family members, ensuring comprehensive protection and support.

The Role of Life Insurance in Family Security

Life insurance is a critical component of a family’s financial safety net. It provides a tax-free lump sum to beneficiaries upon the policyholder’s death, which can be used to replace lost income, cover outstanding debts, fund children’s education, or ensure a spouse’s financial stability. For families, this ensures that even in unforeseen circumstances, long-term financial security for families remains intact, allowing survivors to maintain their lifestyle and achieve future goals without financial hardship.

Planning for Children’s Education and Inheritance

While retirement is a primary goal, many families also prioritize their children’s education. 529 plans offer a tax-advantaged way to save for college, often with state income tax deductions. Integrating college savings with retirement goals requires careful balancing and prioritization. Furthermore, estate planning ensures that your accumulated wealth is distributed according to your wishes, covering inheritance rights and establishing trusts for minor children or dependents with special needs. This foresight protects your legacy and prevents potential family disputes.

Considering Elder Care and Multi-Generational Support

The rising cost of long-term care for elderly parents or other dependents poses a significant challenge. Long-term care insurance can protect a family’s assets from being depleted by these expenses. For multi-generational households, a comprehensive plan must also factor in potential financial support for elderly parents or adult children who may require assistance, highlighting the interconnected futures within a family unit. This might involve creating dedicated funds or adjusting retirement projections to accommodate these responsibilities, demonstrating a commitment to family well-being.

What success looks like: The Miller family, through meticulous planning, established both a robust 401(k) and a fully funded 529 plan for their two children. When the eldest chose an out-of-state university, the tuition was covered without touching their retirement savings, and a modest life insurance policy provided peace of mind, knowing their children’s financial future was secure regardless of unforeseen events.

[INLINE IMAGE 2: an infographic showing different family scenarios (young family, middle-aged family with dependents, retired couple) with corresponding financial planning considerations like 529 plans, life insurance, and long-term care]

See our detailed guide on Tailoring Retirement Plans to Unique Family Needs.

Navigating Tax Implications for Family Retirement Strategies

A sophisticated understanding of tax implications is crucial for maximizing your family’s retirement savings and ensuring efficient wealth transfer. Strategic tax planning can significantly impact the net amount of money available to your family in retirement.

Understanding Tax-Deferred vs. Tax-Free Growth

Retirement accounts generally fall into two categories: tax-deferred (Traditional 401(k), Traditional IRA) and tax-free (Roth 401(k), Roth IRA, 529 plans for qualified education expenses). Tax-deferred accounts allow contributions to grow without annual taxation, with taxes only levied upon withdrawal in retirement. Tax-free accounts, conversely, use after-tax contributions, but qualified withdrawals are entirely free of federal income tax. For families, the choice between these often depends on current versus projected future income tax brackets, allowing for optimized tax efficiency.

Strategic Withdrawal and Tax-Loss Harvesting

Once in retirement, a well-thought-out withdrawal strategy can minimize tax liabilities. This might involve strategically drawing from different account types (taxable, tax-deferred, tax-free) in varying amounts each year to stay within lower tax brackets. For families with taxable brokerage accounts, tax-loss harvesting—selling investments at a loss to offset capital gains and potentially ordinary income—can be a valuable strategy to reduce current tax burdens and preserve more capital for the family’s future.

See our detailed guide on Advanced Tax Strategies for Family Retirement.

Common Mistakes to Avoid in Family Retirement Planning

Even with the best intentions, families can fall prey to common pitfalls that undermine their long-term financial security. Being aware of these errors is the first step toward successful household retirement preparation.

- Underestimating Healthcare Costs: One of the most significant oversights is underestimating the escalating cost of healthcare in retirement. Medicare does not cover all expenses, and long-term care can be prohibitively expensive. Failing to budget adequately for these can quickly deplete retirement savings.

- Ignoring Inflation’s Impact: Many families calculate their retirement needs based on today’s purchasing power, forgetting that inflation will significantly erode the value of money over decades. What costs $100 today might cost $200 or more in 20 years.

- Inadequate Insurance Coverage: Insufficient life, disability, or long-term care insurance leaves a family vulnerable to unexpected events that can derail even the most robust financial plan.

- Poor Communication and Lack of Shared Goals: When spouses or family members aren’t on the same page regarding retirement goals, risk tolerance, or spending habits, it creates discord and inefficiency in planning.

- Starting Too Late: The power of compound interest is immense. Delaying retirement savings, even for a few years, can dramatically reduce the final nest egg, forcing families to play catch-up later.

- Being Too Conservative or Aggressive: An overly conservative investment strategy might not generate enough growth to beat inflation, while an overly aggressive one could expose the family to unacceptable risk, particularly as retirement nears.

- Failing to Account for Dependents’ Needs: Neglecting college savings, special needs trusts, or elder care costs within the broader retirement plan can create unexpected financial burdens.

What failure looks like: The Johnson family, despite earning a good income, delayed serious retirement planning until their mid-50s, prioritizing immediate gratification and their children’s expensive extracurriculars. They severely underestimated healthcare costs and failed to account for inflation. By the time they retired, their savings were insufficient to maintain their desired lifestyle, forcing them to downsize significantly and continue working part-time, straining their marital harmony and impacting their ability to leave a legacy.

See our detailed guide on Avoiding Common Retirement Planning Traps.

Building Your Family’s Comprehensive Retirement Plan (Step-by-Step)

Creating a robust strategy for your family’s future financial security requires a structured approach. This step-by-step guide helps you navigate the process effectively.

- Assess Your Current Financial Situation: Gather all relevant financial documents, including income statements, expense reports, debt records, investment account statements, and insurance policies. Understand your current net worth and cash flow.

- Define Shared Family Retirement Goals: As discussed earlier, establish clear, specific, and mutually agreed-upon objectives for your retirement lifestyle, considering both financial and non-financial aspects.

- Calculate Your Retirement Needs: Estimate how much money your family will need to live comfortably in retirement, accounting for inflation, healthcare, leisure, and any anticipated family support (e.g., elder care or future support for adult children). Utilize online calculators and consider consulting a financial advisor.

- Choose the Right Financial Vehicles: Based on your goals, risk tolerance, and tax situation, select a diversified portfolio of retirement accounts (401(k)s, IRAs, Roths, etc.), as well as relevant insurance products and college savings plans.

- Implement and Automate Your Savings: Set up automatic contributions to your retirement and other savings accounts. Consistency is key, and automation ensures you “pay yourself first.”

- Create an Estate Plan: Ensure your wills, trusts, and beneficiary designations are up-to-date and reflect your wishes for asset distribution and guardianship for any minor dependents.

- Develop a Contingency Plan: Consider scenarios like job loss, illness, or market downturns. Build an emergency fund and review insurance coverage to mitigate risks.

See our detailed guide on A Step-by-Step Guide to Family Financial Planning.

Reviewing and Adapting Your Family’s Retirement Strategy

A family’s financial life is dynamic, with changing circumstances that necessitate regular review and adaptation of its retirement strategy. This ongoing vigilance ensures your plan remains relevant and effective.

Life events such as marriage, the birth of children, career changes, divorce, or the onset of health issues can significantly impact your financial projections. Market fluctuations, changes in tax laws, or shifts in personal priorities also demand re-evaluation. Schedule annual reviews, and certainly, revisit your plan after any major life event. Adjust contribution amounts, rebalance your investment portfolio, update beneficiary designations, and reassess your risk tolerance. The goal is to ensure your household retirement preparation continues to align with your evolving goals and current realities, safeguarding your long-term financial security for families.

See our detailed guide on Adapting Your Financial Plan to Life Changes.

Conclusion: Securing Your Family’s Financial Future

Embarking on comprehensive retirement planning for families is one of the most significant investments you can make in your collective future. It’s a journey that demands open communication, strategic decision-making, and consistent effort, but the rewards are profound: financial independence, reduced stress, and the freedom to pursue shared dreams in your golden years. By understanding core principles, leveraging appropriate financial vehicles, addressing unique family needs, and diligently avoiding common pitfalls, you can build a robust plan that ensures enduring peace of mind. Remember, your financial future is not a static destination but an evolving landscape requiring continuous care and adaptation. For personalized guidance tailored to your unique family circumstances, consulting a qualified financial advisor is an invaluable step.

Sources & References

- Internal Revenue Service (IRS). Publication 590-A, Contributions to Individual Retirement Arrangements (IRAs). www.irs.gov/publications/p590a

- U.S. Securities and Exchange Commission (SEC). “Saving and Investing for Retirement.” www.investor.gov/retirement-and-planning/saving-and-investing-retirement

- Financial Industry Regulatory Authority (FINRA). “Retirement Planning.” www.finra.org/investors/retirement

- Kitces, Michael. “The Ultimate Guide To Retirement Planning & Financial Planning.” Kitces.com. www.kitces.com/blog/guide-retirement-planning-financial-planning-tools-software-strategies/

Reviewed by Dr. Samuel Okoro, Bioethics Professor & Community Advocate — Last reviewed: March 30, 2026